Texas Irrigation and Sprinkler Installer Insurance

See How We're Different

or call us: (855) 359-9324

A single broken pipe that floods a client’s living room, or a trench collapse that injures a crew member, can erase months of profit for a Texas irrigation business. Licensed irrigators in Texas complete intensive training, classroom education, exams, and ongoing continuing education every few years, which shows how seriously the state takes proper system design and installation

according to professional irrigator licensing guidance. Insurance should match that same level of professionalism and protection.

Why Texas irrigation and sprinkler installers need specialized protection

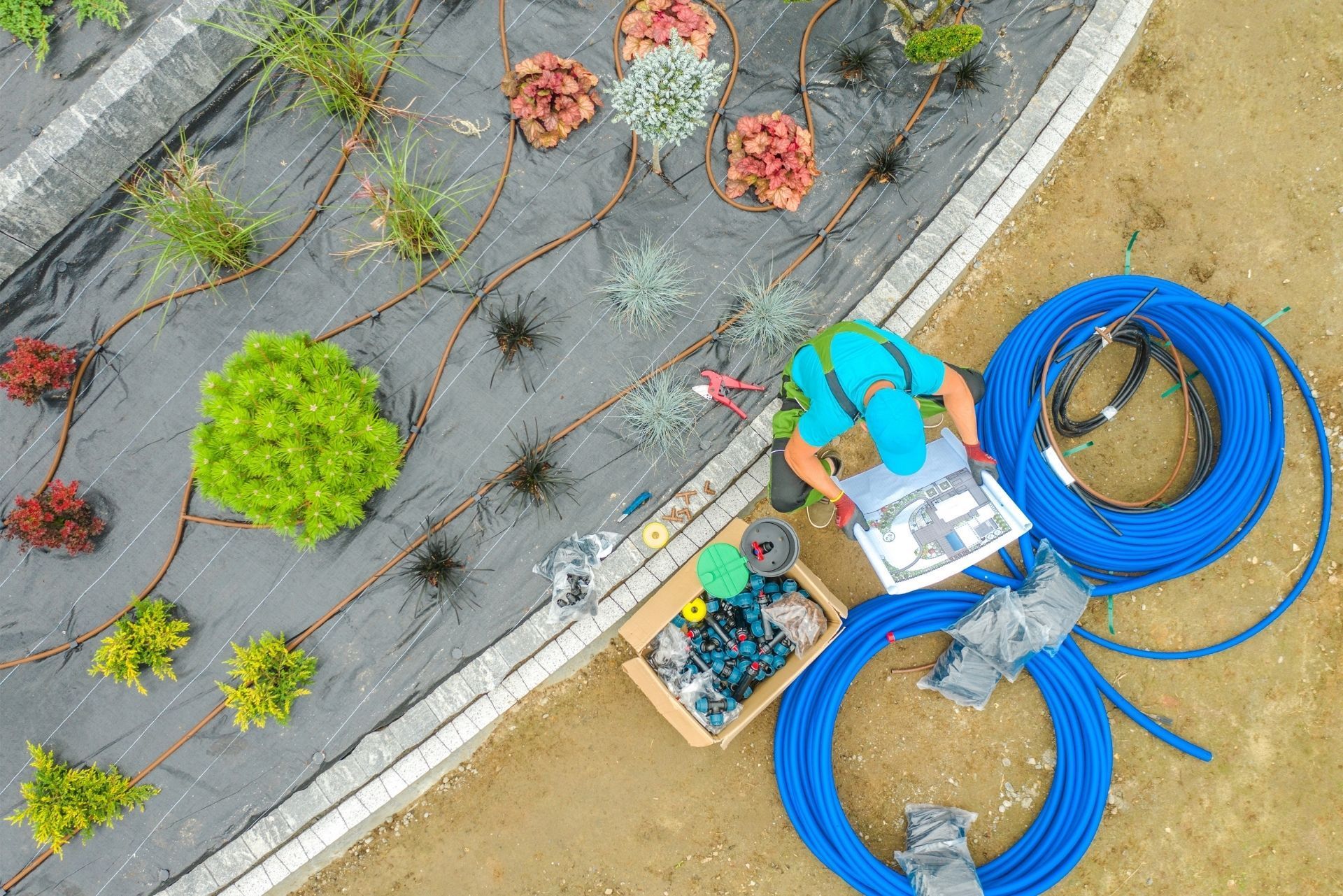

Irrigation and sprinkler work looks simple from the outside. In reality, it blends plumbing, electrical components, trenching, landscaping, and sometimes even concrete cutting. That mix creates unique risks that general contractors or landscapers may not face as often. A cracked foundation from poor drainage, a backflow failure contaminating a water supply, or an employee injured in a ditch can quickly turn into a costly claim.

Texas adds extra pressure because the work does not stop at a neat subdivision lawn. Installers service large rural properties, commercial complexes, athletic fields, and municipal parks. Each type of site brings different exposure. A misaligned golf course head might only annoy golfers, but an overwatered commercial sidewalk can trigger slip and fall injuries, and a failed agricultural system can destroy crops. Without thoughtful insurance, the business, its owner, and often the owner’s personal assets can be exposed.

Many irrigation contractors rely on a patchwork of basic policies picked up over the years. That approach often leaves gaps. The goal of this guide is to map out how coverage should work for Texas irrigation and sprinkler installers, so the insurance program actually reflects the risks out in the field.

Core insurance policies every Texas irrigation contractor should consider

Building coverage around an irrigation or sprinkler operation starts with a core group of policies. These are the protections that handle most of the injuries, property damage, and business interruption problems that can show up on any project. From there, specialty add ons round out the plan so it fits how a particular business works.

Not every contractor will need every option below, especially smaller operations or seasonal crews. Still, it helps to understand what each policy does. That way, it is possible to choose intentionally instead of discovering a gap after a claim hits.

General liability insurance for irrigation and sprinkler work

General liability is often the first policy a client or general contractor asks to see. For irrigation and sprinkler installers, it is usually the foundation of the insurance program. This coverage helps pay for third party bodily injury and property damage the business is legally responsible for. It can also help with certain personal injury claims, like alleged damage to reputation in your advertising.

In practical terms, general liability responds when a sprinkler head cracks a window, a trench trip injures a homeowner, or an overspray issue damages a neighboring property’s landscaping. Many municipalities and HOAs in Texas will not allow work to start without proof of this coverage. For subcontractors, general liability is often a non negotiable requirement to get on the job roster.

Workers compensation and employee injury protection

Any irrigation contractor using employees, even part time or seasonal, needs a plan for workplace injuries. Workers compensation is the standard approach in most of the country. In Texas, the workers compensation market is considered one of the largest and most stable segments of the state’s property and casualty sector, with the system ranked as a leading market nationally according to the 2025 Texas Workers Compensation Market Report. That stability matters when choosing long term coverage for growing crews.

Trenching, operating machinery, lifting pipe bundles, working in extreme heat, and driving between job sites create constant injury potential. Even a careful safety program cannot remove all risk. Workers compensation, where used, can help pay medical bills, a portion of lost wages, and rehabilitation costs for employees injured in the course of their work. It also helps shield the business from many types of employee injury lawsuits.

Commercial auto insurance for work trucks and trailers

Irrigation businesses live on their trucks. Vans, pickups, and trailers carry pipe, fittings, controllers, pullers, trenchers, and sometimes mini skid steers. Personal auto policies generally do not cover business use the way an irrigation company needs. Commercial auto insurance fills that gap. It can help pay for property damage and bodily injury the driver causes in an at fault collision, and it can also cover physical damage to the company’s own vehicles when properly arranged.

In Texas, where crews may drive long distances between suburban neighborhoods, rural properties, and commercial campuses, on road risk adds up quickly. A rear end collision on the interstate involving a loaded trailer can create serious injury and equipment losses. Without commercial auto in place, those costs can land painfully on the business.

Tools, equipment, and installation floater coverage

Sprinkler installers rely on a mix of small tools and larger equipment. Hand tools are easy to overlook, but their total value is often significant, especially when including specialized items like pipe pullers, valve locators, or wire trackers. Add in trenchers, skid steers, and compact excavators, and the exposure grows again. Standard property policies may not fully protect items away from a scheduled business location, or while they are in transit.

Contractors equipment coverage, often written as an inland marine policy or endorsement, can help protect tools and machinery wherever the work takes them. An installation floater can extend protection to materials and partially completed systems on the job site before they are turned over to the customer. Together, these coverages help avoid paying out of pocket when theft, vandalism, or certain weather events damage job critical gear.

Business property and combined business owner policies

Many irrigation contractors operate from a yard, small shop, or shared commercial space. That property can house inventory, controllers, backflow devices, fittings, and office equipment that are expensive to replace. Commercial property coverage can help pay to repair or replace covered property after a fire, certain weather events, or other insured losses. When combined with general liability and other key protections in a business owners policy, it becomes a streamlined package that suits many small and mid sized contractors.

For installers who store client records, plans, or expensive controllers on site, business interruption coverage can also matter. When the shop is out of commission after a covered claim, this coverage can help with lost income and certain ongoing expenses, so the business does not grind to a permanent stop while repairs are in progress.

Professional liability and design errors

Texas irrigation and sprinkler installers often do more than follow a set of supplied plans. Many design systems, size zones, specify controller programming, and adjust layouts on the fly as site conditions change. Those decisions carry a professional component. If a design error causes chronic drainage problems, plant death, or water intrusion into a structure, the client may argue that the damage came from faulty professional advice rather than simple workmanship.

Professional liability, or errors and omissions coverage, is designed for those types of claims. It helps address financial losses tied to alleged mistakes in design, consultation, or system planning. For contractors who provide consulting or design build services, combining professional liability with general liability offers broader protection than relying on either policy alone.

| Coverage type | What it mainly protects | Why it matters to Texas irrigators |

|---|---|---|

| General liability | Third party injury and property damage | Required by many HOAs, builders, and cities before work begins. |

| Workers compensation | Employee injuries on the job | Helps pay medical and wage benefits after trenching, lifting, or heat related accidents. |

| Commercial auto | Company vehicles and on road liability | Protects trucks and trailers constantly moving between job sites. |

| Tools and equipment | Portable tools, machinery, and job site materials | Covers trenchers, pullers, and irrigation components away from the shop. |

| Business property / BOP | Buildings, inventory, and office contents | Safeguards the yard, warehouse, and stored irrigation parts. |

| Professional liability | Design and consulting mistakes | Addresses claims from faulty layouts, drainage planning, or water management advice. |

How Texas weather and insurance market conditions shape irrigation coverage

Texas does not offer a gentle environment for pipes, valves, and controllers. Irrigation systems and the people who install them deal with intense heat, periodic freezes, soil movement, high winds, and large hail. Those conditions influence both day to day risk and how insurers view the state. For sprinkler installers, understanding this backdrop helps explain why certain coverages are priced the way they are and why some limits or deductibles may be higher than expected.

Recent data shows that Texas saw hundreds of large hail events in a single year, with more one inch and larger hail incidents than any other state in that period, according to an analysis of hail activity and severe storm trends reported by the Insurance Information Institute. For irrigation contractors, hail can damage vehicles, controller housings, roofs near wall penetrations, and even exposed piping. It also drives up broader property and auto claim costs across Texas, which often feeds into premiums for businesses that operate heavily outdoors.

Homeowners market pressure and client expectations

Many irrigation installers earn most of their revenue from residential work. The cost and availability of homeowners insurance in Texas therefore affects both client expectations and project budgets. Texas has been identified as one of the least affordable states for homeowners coverage, reflecting a mix of severe weather, coastal exposure, and other catastrophe risks that put pressure on insurers and policyholders alike according to the Insurance Information Institute.

Homeowners who feel squeezed by their own insurance costs may be more cautious about any contractor they allow on site. They may demand higher liability limits, ask tougher questions about certificates of insurance, and be less tolerant of mistakes that could trigger a claim. For contractors, that means insurance is not only risk protection but also a sales tool. Being able to clearly explain coverage, limits, and risk management practices can help win business from cautious property owners.

Crop loss, drought, and shifting irrigation expectations

Drought and water restrictions are not abstract issues in Texas. They shape how clients think about irrigation and can influence project design, from smart controllers to drip systems and soil sensors. The financial strain is visible in agriculture, where drought related crop insurance payouts in Texas have risen sharply compared with earlier decades, with average annual payouts increasing several times over recent baselines in the early part of this century as reported in an analysis of drought impacts on crop insurance.

While landscape irrigation contractors do not typically work directly with crop insurance, the same climate pressures push commercial and institutional clients toward more efficient and resilient systems. If a contractor miscalculates watering needs under these tighter margins, the financial fallout from plant loss or soil damage can be significant. Insurance cannot fix a poor design, but professional liability and strong contracts can cushion the financial hit when disputes arise over whether a system performed as promised.

Texas insurance market strength and what it means for irrigation businesses

Texas hosts one of the largest property and casualty insurance markets in the country by premium volume. Recent reporting shows that direct written premiums for property and casualty coverage in the state reached tens of billions of dollars in a recent year, with personal auto accounting for a substantial share of that total according to the 2025 ICT Texas Property and Casualty Market Report. For irrigation contractors, this depth means there are many carriers and policy options, but it also comes with active competition and careful underwriting.

A strong market can benefit irrigation and sprinkler installers in several ways. First, a larger pool of insurers often means more flexibility in tailoring coverage. Carriers may be willing to add endorsements or structure packages specifically for contractors who trench, install backflow preventers, and manage controls. Second, a mature market encourages specialization. Some insurers focus heavily on contractors, while others build expertise in small business packages that fit smaller irrigation firms well.

That said, a large and complex market can be confusing. Two quotes with similar premiums can hide very different exclusions and limits. Working with a knowledgeable agent or broker who understands both Texas risk and irrigation operations can make a noticeable difference in coverage quality for about the same spend.

Workers compensation, crews, and safety culture for Texas irrigators

Even though irrigation installers are known more for sprinklers than scaffolding, the work still carries serious injury potential. Crews operate trenchers and boring equipment, work in hot temperatures, and handle pressurized lines and electrical controllers. Texas has built one of the largest workers compensation systems in the country, with the workers compensation segment ranked among the top markets nationally and a high share of employees covered through private carriers or self insured plans based on data from the 2025 Texas Workers Compensation Market Report.

That environment offers several advantages to irrigation businesses that choose to carry workers compensation. A larger insurer pool can mean more competitive pricing for contractors with good safety records. It also encourages loss control resources. Many carriers provide training materials, job site checklists, and heat stress guidelines written specifically for outdoor trades. For small irrigation companies that may not have a full time safety manager, those tools are valuable.

Insurance alone is not a safety program, though. Irrigation contractors that thrive in Texas tend to integrate claims experience, carrier guidance, and field knowledge into a real safety culture. That may include daily stretch and flex sessions, tailgate talks on trench safety, hydration protocols, and simple practices like color coding utilities on site plans. A strong safety record not only protects people, it can support more favorable workers compensation terms over time.

How much insurance does a Texas irrigation or sprinkler business need

No two irrigation operations look exactly the same. A small team focusing on residential system startups and minor repairs has different needs than a contractor handling design build projects for sports complexes and large commercial campuses. Deciding on coverage limits starts with mapping out worst case scenarios. That means imagining what would happen if an employee suffered a serious injury in a trench, if a misplaced line caused structural damage, or if a truck collision injured several people in another vehicle.

Client contract requirements often set a baseline. Many builders, municipalities, and property managers specify minimum limits for general liability, auto, and sometimes umbrella coverage. Meeting those levels keeps the door open for bigger projects. Beyond that, irrigation contractors should consider the value of property they regularly work around, both buildings and landscaping. Systems serving higher end homes, hospitality properties, or sensitive facilities call for stronger liability protection because potential damages are larger.

It is also useful to think about growth. An installer who plans to add crews, expand into commercial work, or branch into landscape lighting and drainage may find that starting with slightly stronger limits today prevents repeated policy adjustments later. Insurance limits can be raised as the business scales, but doing so before a major incident, not after, is always the better path.

Risk management steps that help control insurance costs

The best way to manage insurance over the long term is to focus on the part that can be controlled: risk. Carriers look at claim history, type of work, crew experience, and safety practices when pricing irrigation contractors. Reducing claims does more than protect people and clients. It often stabilizes premiums and gives the business more options when shopping coverage.

Texas licensed irrigators already operate under training and continuing education expectations that exceed what many homeowners realize. Licensing requirements typically include classroom instruction, examination, and recurring education hours every few years to stay current on code changes and best practices as outlined in guidance for professional irrigators in Texas. Turning that technical expertise into clear field procedures is the next step. Standardizing trench depth, pipe bedding, wiring methods, and backflow installation details reduces both warranty callbacks and claim risk.

Job site practices that reduce liability claims

Most liability problems start with small oversights. An open trench near a homeowner walkway, a missing warning cone around a muddy area, or a forgotten shutoff can all lead to injuries and property damage. Written job site checklists help crews avoid those misses. Items like confirming utility locates, placing barricades, checking for overspray near sidewalks and neighboring buildings, and photographing conditions before and after work create a trail that is useful if a claim arises.

Documented change orders are equally important. Irrigation projects frequently evolve when clients add zones, ask for different heads, or tweak landscaping plans. Without written confirmation of changes, disagreements can emerge about what was promised versus delivered. Clear documentation, tied to signed approvals, keeps many disputes from turning into formal claims.

Vehicle and equipment controls

On the auto side, simple controls go a long way. Formal driver vetting, periodic motor vehicle record checks, and basic defensive driving expectations reduce crash frequency. Enforcing no phone use while driving and reasonable maximum speeds with trailers attached can prevent the kind of collisions that lead to severe injuries and long claim tails. For equipment, locking trailers, using hitch locks, and setting rules about where tools are stored overnight cut theft losses.

Maintenance logs matter as well. Keeping written or digital records of oil changes, brake work, and tire replacement on trucks, and similar logs for trenchers and skid steers, can be valuable if an accident triggers a liability investigation. Those records show that the business took reasonable steps to keep equipment safe to operate.

Working with an insurance professional who understands irrigation

Insurance language can be dense, and policy forms vary by carrier. An agent or broker familiar with contractors and, ideally, irrigation specifically can flag gaps the business owner might miss. For example, some policies may limit coverage for underground work, damage to property being worked on, or water damage arising after project completion. Those are central issues for sprinkler installers. Reviewing these details before a loss gives space to make changes.

When meeting with an insurance professional, it helps to bring real information, not just a business name and revenue figure. Details like the mix of residential versus commercial jobs, average project size,

use of subcontractors, and any design or consulting services all influence recommended coverage. Sharing safety practices, training programs, and past claim handling can also support better placement and pricing.

Frequently asked questions about Texas irrigation and sprinkler installer insurance

Contractors often share similar questions once they start digging into their coverage. The answers below address common concerns from Texas irrigation and sprinkler professionals.

Is general liability enough for a small irrigation business working only on homes?

General liability is a critical starting point, but it rarely covers everything a residential irrigation contractor needs. Even small businesses should consider coverage for tools and equipment, commercial auto for work vehicles, and some form of employee injury protection once helpers or crews are involved.

Do I need professional liability if I mostly follow manufacturer specs?

If the work includes system layout, zone sizing, or adjustments to plans based on site conditions, there is a professional component, even when using manufacturer guidelines. Professional liability helps protect against claims that the design or advice, not just the physical installation, caused a financial loss.

Can I rely on my personal auto policy for my irrigation work truck?

Personal auto policies generally are not built for regular business use, especially when carrying tools, materials, and employees. Most irrigation contractors are better protected with a commercial auto policy that reflects how their vehicles are actually used.

What if I use subcontractors for trenching or specialized work?

Subcontractors add flexibility but also create insurance questions. Contractors should require proof of coverage from subs, including general liability and any applicable workers compensation, and have their own policies reviewed to make sure they handle subcontracted work correctly.

How often should I review my insurance program?

An annual review is a good baseline, but a meaningful change in operations, such as adding crews, expanding into commercial work, or buying larger equipment, is also a good time to revisit coverage. Waiting until renewal after a big business change can leave gaps.

Will investing in safety training really lower my premiums?

Strong safety programs reduce claims, and over time, a better loss history can support more favorable pricing and coverage options. Some insurers also offer credits or additional resources to contractors who demonstrate active safety efforts.

Before you go: key takeaways for Texas irrigation businesses

Texas irrigation and sprinkler installers operate in a state where weather, water, and insurance markets are all under pressure. Drought related payouts in agriculture and rising severe weather costs have made insurers more cautious in many lines of business, highlighting the importance of thoughtful risk management for any operation tied to outdoor work and water use as documented in recent reporting on climate and insurance impacts in Texas. That backdrop makes a well built insurance program even more important, not less.

For irrigation contractors, the essentials are clear. Understand the core coverages, from general liability and workers compensation to commercial auto and equipment protection. Decide on limits based on real world scenarios, client requirements, and growth plans. Use Texas specific factors, like hail exposure and drought driven design demands, to shape both coverage and field practices. Finally, pair insurance with a living safety culture and consistent documentation so when something does go wrong, the business has both financial backing and a strong story to tell.

With that approach, a Texas irrigation or sprinkler business is not just meeting minimum requirements. It is protecting its crews, its clients, and its reputation, laying the groundwork for steady growth in a demanding but opportunity rich market.

About The Author: Mark Braly

As President & CEO of Braly Insurance Group, I’ve built my agency since 1997 on the promise of protecting what matters most for families and businesses across Texas.

With a finance degree from Oklahoma State University and nearly three decades in the industry, I lead a team that offers tailored, local insurance solutions—whether it’s specialized commercial coverage or personal protection.

Outside the office, you’ll find me on the golf course or playing piano, always energized by time with my family and my commitment to giving back through organizations like CASA McKinney.

Testimonials

Real Insurance Clients with Honest Reviews

Braly agency was very honest and professional to work with. They have many resources to choose from and are a full service Insurance Agency. I highly recommend! Caden provided excellent and knowledgeable service throughout the process.

Louis G.

Insurance Client

I have been with the Braly Group for years. Their attentiveness gratitude and all around a good group to take care of your insurance and others needs.

Thanks for being amazing,

Jeff D.

Insurance Client

I have been with the Braly Insurance Group for over 10 years! Absolute professionals who definitely take care of you personally. I trust the Braly Group to give me the best product and price for my insurance needs!

Doug F.

Insurance Client

Everyone at Braly Insurance is always friendly & helpful. Whether you need to file a claim or make changes to your policy they are there to help with whatever you need.

Terry B.

Insurance Client

Business Insurance

Commercial Insurance Policies

General Liability Insurance

Comprehensive protection against lawsuits and other common business risks.

Workers Comp Insurance

Coverage for medical expenses and lost wages due to workplace injuries.

Commercial Property Insurance

Protect your business property from damage, theft, and natural disasters.

Commercial Auto Insurance

Insurance for vehicles used in your business operations, covering accidents and damages.

Professional Liability Insurance

Protection against claims of negligence, errors, and omissions in your professional services.

Industry-Specific Insurance

Businesses We Serve

Plumber Insurance

Electrician Insurance

Hotel Insurance

Software Insurance

Restaurant Insurance

Manufacturer Insurance

FAQs

Frequently Asked Question About Braly Insurance Group

What's the difference between an independent insurance agent and a captive agent?

Independent insurance agents, like those at Braly Insurance Group, offer a wide range of insurance products from multiple companies, allowing them to compare policies and find the best fit for your needs. Captive agents are tied to a single insurance company and can only offer products from that provider. Choosing an independent agent in Texas provides access to a broader selection of options, ensuring a more personalized and cost-effective insurance solution.

Why should I choose an independent insurance agent in Texas?

Opting for an independent insurance agent in Texas means receiving personalized, unbiased advice across a wide spectrum of insurance options. Independent agents source policies from multiple companies, tailoring coverage to your specific needs, often at more competitive prices. They possess a thorough understanding of local insurance requirements and risks, ensuring your coverage is both comprehensive and relevant to Texas.

What are the typical insurance types offered by independent agents in Texas?

Independent agents in Texas typically provide a broad range of insurance types, including homeowners, auto, life, and umbrella policies, as well as specialized coverage like motorcycle and condo insurance. They offer customized solutions for various situations, ensuring you have access to policies that match your specific needs, whether you're protecting your family, home, vehicle, or personal assets.

What's the cost to collaborate with an independent insurance agent in Texas?

Engaging with an independent insurance agent in Texas usually doesn't involve any direct costs or fees for their advisory services. Agents earn commissions from the insurance companies for the policies they sell, allowing you to benefit from their expertise and personalized service without incurring additional expenses. Their objective is to secure the best coverage for you at the most competitive rates, aligning with your financial and insurance needs.

Why should I partner with a local independent insurance agent?

Partnering with a local independent insurance agent offers numerous advantages. They have a profound understanding of Texas' unique insurance needs and challenges, providing advice and solutions tailored to the local context. Local agents are readily available for face-to-face meetings, offering a level of personalized service that larger, non-local agencies can't match. Their commitment to the community means they're dedicated to finding the best insurance solutions for their neighbors, adding a personal touch to their professional services.

Personal Insurance options

Our Complete Range of Personal Insurance Solutions

Home Insurance

Protect your home with comprehensive coverage tailored to your needs. Secure your peace of mind today.

01

Car Insurance

Drive confidently with our customizable auto insurance plans designed for every driver and vehicle.

02

Boat Insurance

Enjoy your time on the water with our reliable boat insurance, covering damages and liabilities.

04

RECENT POSTS

Get the Latest Updates

Contact Us